It has been just over a year since Northwestern Mutual acknowledged that it was struggling internally due to the continuous low interest rate environment. In early 2017 the company made it clear that it needed to “streamline” and “restructure”.

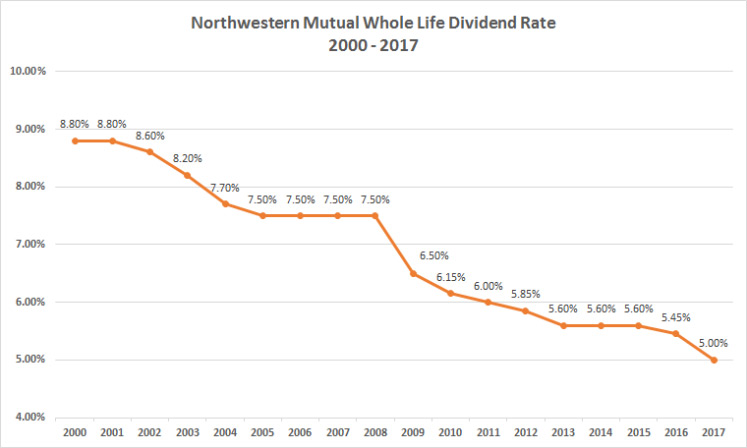

In October 2016 Northwestern Mutual reduced their dividend crediting rate again from 5.45% to 5%. Since 2008, Northwestern Mutual has reduced their dividend rate by 2.50%. The chart below shows their dividend rate drop since 2000.

Source: https://www.northwesternmutual.com/how-we-determine-dividends/

Lowering the crediting rate even half a percent will result in significant changes for all policy holders including:

1.policies requiring more premium dollars to stay in force and meet original projections

2.Policy will lapse (terminate)

3.Automatic loans from the death benefit will be drawn if premiums are not paid accordingly

These are just a few problems but the dividend drop will have a substantial impact on policy holders. This has caused concern in the whole life insurance industry because Northwestern Mutual represents a significant portion of the market share in several midwestern states, and many major US cities with younger affluent owners. The other glaring problem is many affluent professionals purchase policies with the intent of taking distributions out of their policy for income in retirement and holding a death benefit until age 100.

If you own a Northwestern mutual whole life policy it is highly likely your policy is not performing as originally projected when it was purchased. Fortunately for policy holders there are options available to improve a policy.

Start by having an independent insurance advisor review your policy

An independent insurance advisor is typically not affiliated with any specific insurance company. Therefore the advice you receive will be objective and un-biased towards a specific product or carrier.

As a result of a policy review there is a high probability a policy holder can increase their cash value, increase their income from the policy, increase the death benefit, or reduce the amount in premium needed to keep the policy in force.

One firm in particular, Tippett Moorhead and Haden has tackled this issue head on. They are an independent firm with access to proprietary life insurance products. They have proven to effectively advise policy holders on how to replace their existing whole Life policies with a policy that generates more retirement income, larger death benefits, or both.

Conclusions

No one can predict exactly what will happen to Northwestern Mutual as it restructures and repositions itself in the industry. If you want to make sure your insurance will be there for you no matter what happens, the safest thing to do is to re-evaluate exactly which policies you hold and what they do for you. For that, you will need an insurance review from an independent life insurance advisor, or you simply won’t get a full menu of options available.

File # 1685-2018